847-903-7578

Scott Kendall Owner

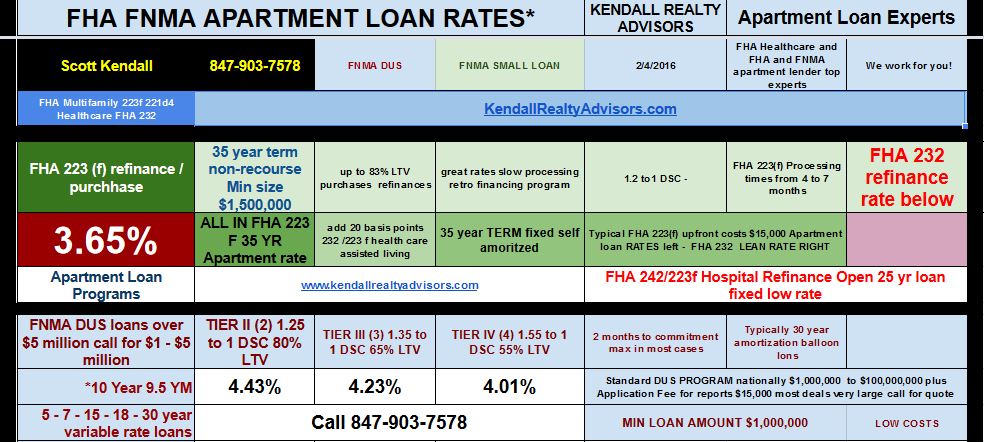

Apartment Loans Commercial Mortgages Chicago, Nationally, Small Apartment Loans, FHA 223 F,FNMA DUS, FNMA Small Apartment Loan rates news

10 Year

|

1.75% |

30 year treasury record low rate #Apartment #Loan http://t.co/mJiPIBJOrM FHA FNMA #rates https://t.co/jbELAmgEGp

— Apartment Lender (@lenderapartment) January 30, 2015